Never Retire - How Conventional Retirement Advice Sets Us Up To Fail (And Live Boring Lives)

Never Retire - How Conventional Retirement Advice Sets Us Up To Fail (And Live Boring Lives)

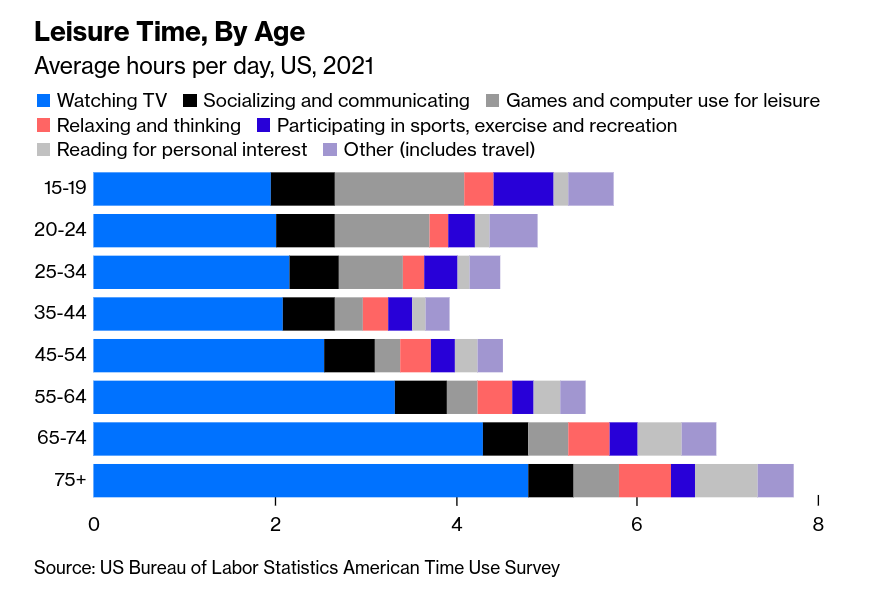

35-44 year olds enjoy less leisure time than they have in a long time

Every single day, multiple articles like this one get published on the internet.

After working for decades, retirement should be all about relaxing and getting some well-earned peace and quiet.

The introductory sentence paints a not-so-nice picture of life before retirement. You worked so much you rarely, if ever experienced peace and quiet.

The solution: Move to West Virginia, Arkansas, Iowa, Oklahoma, or Mississippi. Because they’re relatively cheap places to live. You might be able to get by on your meager savings + Social Security there.

No offense to anybody from or who lives in those states, but that doesn’t even resemble an attractive option for large swaths of the population.

The target audience for an article like that are people already up against it. They have traditionally retired and worry about outliving their money.

It’s this fate many of us are trying to avoid.

So the earlier we realize we might Never Retire—and deal with it—the better.

However, the primary theme prevading conventional financial media on how to deal with this comes down to two words—save more.

Here’s how much you should have saved by age 30, by age 40, by age 50, and so on. If you don’t have this much, increase your savings.

This advice only reinforces and perpetuates the pessimistic view of life before retirement. Those 40 or so years prior to turning 65 should be reserved for working yourself into the ground—particularly if you’re behind on your savings—so you can earn that, to-this-point, elusive peace and quiet.

No fun. Not the type of life I want to live, as someone who just turned 47 and absolutely doesn’t have and will not have enough saved for a traditional retirement.

But it’s not just subjectively bad advice people who value leisure time don’t want to hear.

In many cases, it’s objectively bad advice. It puts you on the personal financial hamster wheel—retirement style—and potentially sets you up to fail.

For example, in an April installment of the Never Retire newsletter, we looked at the average retirement savings by generation:

Total household retirement savings among all workers is $93,000 (estimated median). Baby Boomer workers have the most retirement savings at $202,000, compared with Generation X ($107,000), Millennials ($68,000), and Generation Z ($26,000) (estimated medians).

Let’s expand on what we discussed in that article with some back-of-the-envelope math.

Let’s assume you’re an older millennial/younger GenXer in the 35-44 demographic. This age group comes up again in a minute.

So, at around age 40, you have $68,000 saved for retirement. Wishful thinking for many people, but that’s okay. It makes this illustration more effective.

Let’s assume this 40-year old started saving regularly at age 25. In 15 years, they accumulated $68,000.

This means, at a 6% annual rate of return, they were saving about $233 a month.

Keep that pace for another 25 years—to age 65—and you have approximately $466,337.

Now, this is an impressive chunk of money.

$466,337.

However, it’s clearly not enough to fund a traditional retirement from 65 years old on.

If you only live for 20 years, that $466,337 gives you $23,316 a year. Not bad. But also not great.

25 years and $466,337 provides $18,653 a year.

30 years and $466,337 generates $15,544 a year.

I make my personal projections—knock on wood—based on living to 100.

If you’re renting or carry a mortgage in retirement, this puts you in a precarious situation. Just a $500 or $1,000 monthly housing payment eats up half or more of your cash every year. If you want to have a life—like the people in the picture at the beginning of this article—you’re just screwed.

It doesn’t take a mathematican with a minor in rocket science to see this is not a favorable financial position in old age.

This is why one of the main things we do in this newsletter is explore strategies for this, presumably, common situation: You saved/make decent or better money, but not nearly enough to fund traditional retirement. And you don’t want to live to work.

Thus the recent borderline obsession with eliminating your housing payment.

However you decide to go about it, if you see the writing on the wall and it says I’ll probably Never Retire don’t double down on traditional retirement. Even though it’s the course most of the experts suggest you chart, it really makes no sense.

Find out how to best use the money you have managed to save in conjunction with a way to generate meaningful cash flow into relative old age, whether it’s through some form of work (preferably flexible and freelance), becoming a landlord, or a mix of both. Or something else entirely.

Thankfully, this is the path an increasing number of us are taking. We’re not holding onto the hope of a traditional retirement. We realize it’s a futile effort likely to disappoint.

We’re embracing Never Retiring as a favorable alternative to traditional retirement. Because traditional retirement often requires you to sacrifice your prime years—by working too hard and too much—to subsidize life post-age 65. When, thanks to how you devoted yourself to the grind for 40 years, you might not be physically and mentally capable of enjoying that well-earned peace and quiet.

Back to the 35-44 year olds we mentioned earlier.

Recent US Census data shows that this age group—older millennials/younger GenX—have less leisure time than any other age group and less than they did 20 years ago.

Do you think this lack of leisure time—especially in the travel, reading, and sports/exercise/recreation categories—has anything to do with the prevailing mindset on retirement?

How about—

Work less now so you can work less longer across the lifespan.

Participate in active leisure time—multiple times a week—to help preserve your physical and mental health.

Organize your money and work around your life, not the other way around.

Find the floor on your cost of living. Aim to eliminate or greatly reduce your housing expenditure.

These are themes, mindsets, and strategies that can help set up the type of life you wanna live now and for the duration.

Another fabulous thought provoking write up. I love reading these in the morning over some fresh Java. Sets the tone for my day.